![<?echo $_SERVER['SERVER_NAME'];?>](/template/twentyseventeen/skin/images/header.jpg)

2012 was one of the toughest years for the solar industry. In fact, in the past 18 months, the market has been swayed by the growth expectations of the solar industry. At the end of 2011, some companies worried that the end market demand in 2012 would decline as in 2011, thus amplifying the challenges of the industry in 2012. The good news is that global solar demand has not declined in 2012, but it has not grown to significantly reverse the imbalance between supply and demand. The decline in average sales prices has driven demand to rise significantly (especially in emerging markets).

In 2012, some new business models and strategies also appeared. Before 2012, most manufacturers only focused on manufacturing, becoming the best supplier through vertical integration with upstream, or enhancing brand recognition through the establishment of market channels; and now, corporate strategies are increasingly concentrated In project development, in order to increase gross profit margin or guarantee the shipment of self-produced modules. The rise of the Chinese market has further stimulated this strategic shift, which contains huge challenges and potential rewards.

Another thing worth looking forward to is that there will be considerable growth in emerging markets, and the demand in the end market will be expanded to more countries, thereby helping to reduce the risk of demand decline caused by changes in preferential policies. Many trade dispute investigations that began in 2012 will eventually end in 2013, and are likely to significantly change the supply chain pattern of the solar industry.

To this end, solar companies have been planning various business strategies and company activities since 2012, most of which are defensive in order to create sustainable business models and survive in 2013 and beyond. Although these processes are painful and face various challenges, new opportunities are expected to emerge in the next few years.

First-tier manufacturers develop to the downstream terminal market

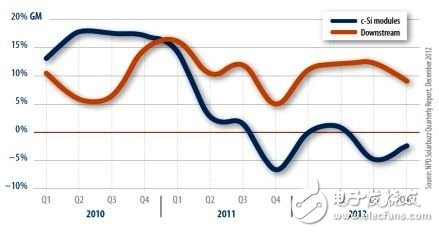

In the past two years, falling sales prices have seriously affected various types of manufacturers and caused some manufacturers to seek new profits downstream. The trends shown in Figure 1 can explain why the transition to project development is attractive and when the business model changes. Since 2011, the continuation of quarterly module gross profit margins has led many companies to start to care about the company's development strategy. Then in 2012, they carried out a strategic transformation, that is, manufacturers who simply manufacture began to enter downstream projects.

In 2012, almost all Chinese first-tier manufacturers began to enter the field of project development to varying degrees. The scale of the project development that most manufacturers are involved in is still relatively small, usually only a few hundred megawatts, and the proportion of the confirmed revenue to the total revenue is also low. However, there are also some manufacturers that are more actively transforming and plan to increase the revenue of downstream projects to more than half of the total revenue in 2013.

Figure 1 Weighted average gross profit margin of polysilicon modules and downstream projects

(Source: NPD Solarbuzz)

Some people in the industry regard this move to downstream as a way for many struggling companies to learn from each other. However, any transition to a new business model is risky, no matter how efficient an enterprise is in manufacturing. There is no guarantee that an enterprise can succeed in the field of project development.

One of the most important challenges in project development is to establish a reliable and efficient operating mechanism, which may not be directly transferred from the manufacturing background. An in-depth understanding of the market, policies, and regulations in which the project is located is crucial. Any mistake will have an impact, ranging from project extension to contract cancellation.

This also poses another challenge to performance goals and financial performance, because project delays of only a few weeks will cause revenue to be unrecognized and enter the corresponding quarterly statements, making the balance between project reserves and manufacturing more difficult. At the same time, it also creates the possibility of direct competition with the first customers, thus jeopardizing the supply relationship that the first customers have.

In addition, many downstream transformations have come from the launch of the Chinese market. There is a risk, because the Chinese market is still highly dependent on policy-driven, and only continuous support from the Chinese government can maintain rapid growth. Thankfully, the increasing solar installation target and various preferential policies covering different customer classification markets indicate that this support is increasing.

However, this growth does not benefit all companies in the industry. Only companies with both strength and relationship can profit from the growth of the market. At the same time, the entry of so many first-tier manufacturers has created a similar upstream situation in the downstream industry, that is, growing production capacity and intensified competition are concentrated in one category market, resulting in prices falling to gross double-digit levels.

China's rising up

The rise of the Chinese market is mainly to provide opportunities for Chinese companies. This fact may not be surprising, but it may cause many changes in the supply chain. As mentioned earlier, Chinese companies dominate the growth of downstream demand in China. However, when considering the needs of the Chinese market at different stages from January to December, there are certain challenges.

Generally speaking, when the demand in any market is concentrated in a certain season, it may cause an imbalance in the supply of upstream manufacturers. Previously, the global solar market was mainly concentrated in the second half of the year, because the reduction in subsidies at the beginning of each year in Europe would lead to an increase in demand in the fourth quarter and developers ’installation. This model still existed in 2012. However, as shown in Figure 2, it was mainly affected by the growth of the Chinese market in the second half of the year, especially in the fourth quarter of 2012.

Figure 2 Contribution of the Chinese market to global demand in each quarter of 2012 ~ 2013

(Source: NPD Solarbuzz)

The main problem of this concentrated release of demand is that manufacturers must bear the risk of production and holding a large amount of inventory in the first half of the year in order to profit when shipments rise in the second half of the year. In an environment of declining prices, the strategy of holding a large amount of inventory will face the risk of inventory price loss and decline in gross profit margin. Companies facing the Chinese market already had this experience in 2012 and had to decide whether to stick to a similar strategy in 2013.

Such industrial development also provides opportunities for companies that do not focus on a single unstable market situation (such as China). The global solar market outside China ’s annual demand is expected to show a steady upward trend in each quarter of 2013, which will help companies plan Draw output and shipment levels.

Aluminum Profiles Materials and features:

1, the shape led jewelry counter lamp housing are V-shaped, U-shaped and triangle, so the jewelry counters led lamp housing, also known as V-groove, U-groove and triangular-shaped groove;

2, Sichuan and spread of new energy production can be equipped with plug, 90 degree angle, angle of 135 degrees, 180 degrees straight through led jewelry counter lamp housing, 6063 GB of raw materials are all aluminum, high purity aluminum, quality assurance, all through the testing and certification;

3, surface gloss, uniform oxide film, bright color, color uniformity, corrosion resistance;

4, the appearance of fine, beautiful, overall product design scientific and rational, durable;

5, high-pressure tensile aluminum shell, good heat dissipation, and diverse styles.

6, product variety, can be customized according to customer demand.

7, the surface may be anodized, electrostatic spraying, gloss treatment

8, streamlined design, the appearance of multilateral tooth design, increase the cooling area, cooling fast.

Aluminum Profiles

Aluminium Profiles,Aluminum Profile For Curtain Wall,Aluminium Profiles For Windows And Doors,Waterproof Aluminium Profiles

Shenzhen Mingxue Optoelectronics CO.,Ltd , https://www.led-lamp-china.com